The party is over in commercial real estate. Here’s what to expect in 2023.

An period of low-priced debt that aided elevate price ranges on lodges, workplace properties and other U.S. business qualities to dizzying new heights has ended.

Better funding fees already were a issue for 2023, with billions of bucks well worth of more mature industrial mortgages coming owing. Including to the woes, prime tech titans, which includes Meta Platforms

META,

in latest months have retreated from splashy business leases.

“You experienced all these massive tech providers signing significant new leases, which was obtaining the current market comfortable with the thought that the office environment sector was going to recover more than the more time time period,” claimed Greg Handler, head of home loan and client credit history at Western Asset Administration.

Now, just one of the few brights places in the near $21 trillion business real-estate market place has become another headwind, Handler said. “It raises serious issues about who is heading to decide up that additional sq. feet, and at what rate.”

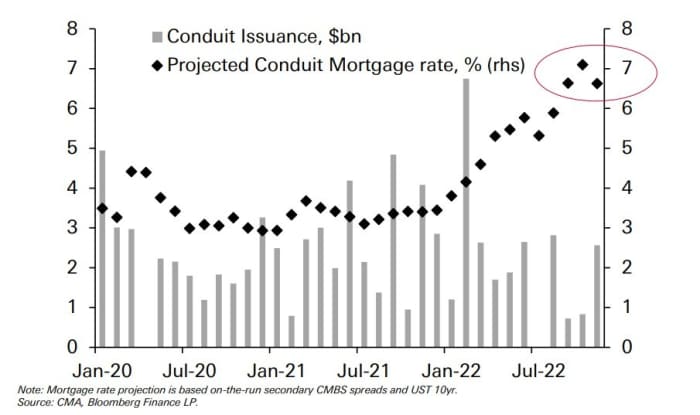

Home puzzle

Insurance plan businesses and financial institutions normally make professional assets loans to keep on their guides, even though Wall Road offers up the credit card debt into bond bargains.

Issuance of bonds, termed business property finance loan-backed securities, or CMBS, has been a driving pressure in residence finance for a long time. But this yr, “conduit” bond issuance backed by many debtors and attributes collapsed as home loan charges topped 7{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7} (see chart), in accordance to Deutsche Financial institution investigate.

Collapse of a crucial home funding supply

CMA, Bloomberg, Deutsche Bank Research

Landlords are inclined to default when credit card debt comes thanks and funding dries up, a scenario that can be exacerbated when a property’s cash flows or valuation falls.

Though general public marketplaces this yr repriced commercial genuine estate significantly lower, non-public markets have still to budge a lot from document amounts, even with historic losses in stocks, bonds and other economic property.

See: Office-residence woes are driving REIT carnage as 2022 shapes up to be 2nd-worst 12 months on file

The Dow Jones Equity REIT Index

DJDBK,

was on tempo to shed 25{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7} this calendar year, a worse drop than the S&P 500 index’s

SPX,

about 17{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7} slide, according to FactSet.

“The even larger challenge, I assume, is likely to be how do the debtors refinance,” mentioned Alan Todd, head of CMBS investigate at BofA Global. “And which is not just on business office. It’s if you are in a residence where by now valuations are reduce, your price is appreciably greater, how are you heading to refinance properly?”

What if costs tumble 30{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7}

Professional residence prices cooled a bit in new months, but nonetheless have been up 7.3{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7} on the calendar year by way of Oct, according to the RCA CPPI index. What’s extra, price ranges had been an eye-watering 123.5{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7} increased from 10 many years back.

Todd at BofA World-wide thinks home charges could fall 20{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7}-30{7e5ff73c23cd1cd7ac587f9048f78b3ced175b09520fe5fee10055eb3132dce7}, then see an uneven recovery. “You’re conversing about a secular, not cyclical, modify for sure property varieties, no matter if those are regional malls or some of the decreased quality offices,” he said. “Some of all those could be relatively problematic.”

Even so, Todd does not foresee a deluge of foreclosures, distress or the magnitude of losses that adopted the 2007-2008 world monetary disaster, since several loan providers now have far more leeway to work with borrowers to hold out out the storm.

Borrowers could also faucet into equity taken out of attributes to fund tenant advancements or to get a new personal loan. “We’ve experienced 10 decades of cash-out refis, so you gotta think they have money they can funds in,” Todd said.

Analysts at Morgan Stanley estimate that some $300 billion in “dry powder” also sits on the sidelines, which probably could be deployed and restrict the slide in property charges.

Though, with sales volumes mostly stuck in a rut, any buyer striving to estimate in which home values may finally shake out is getting a stab in the dim. The Fed also expects to preserve borrowing costs up, right until inflation finds a clear path down.

“There is an approximated $450 billion of loans that will come thanks in each of the following four several years,” said Rich Hill, head of true estate technique and exploration at Cohen & Steers, a authentic assets-targeted financial investment supervisor. “The marketplace is owning to arrive to the reality that the times of inexpensive revenue are absent.”

Still, Hill sees business authentic estate heading into 2023 on relatively sound footing, provided prudence from loan providers in the previous 10 years and his firm’s forecast for internet-earnings and earnings growth to remain better if the U.S. economy sinks into a recession.

“It’s most likely that residence values tumble in the future 12 to 24 months,” he stated. “But in an atmosphere when funds flows are fantastic, I really do not think lenders will offer distressed houses into a difficult market.”